In the previous post in this series, 5 reasons LOBO loans to local councils are a rip-off, Part 1, I explained how the contracts for these long-term loans make them a lose-lose bet for councils. Due to the way the deals are drawn up the council eventually ends up paying too high an interest rate.

In this post I’ll set out another two reasons why LOBO loans are a terrible deal for the public purse, again keeping the language as non-technical as possible. The second reason is that, LOBO loans, like all loans that councils take out from banks, suck money out of the public sector. Thirdly, LOBO loans are a lot more expensive to arrange than equivalent loans from central government.

2. LOBO loans suck money out of the public sector and into the pockets of bankers

To recap, councils essentially have two options when they need a load of cash to build a school, library or undertake any other kind of big project: they can borrow money from the Public Works Loan Board (which is under the control of the Treasury) or they can go to the private sector.

As Abhishek Sachdev pointed out in the Channel 4 Dispatches documentary ‘How councils blow your millions’, when a bank sells a LOBO loan to a local authority it books a hefty chunk of profit on the first day. In the documentary the example is given of a £15 million loan that Walsall Council took out from Barclays. Sachdev estimates that Barclays would have booked a £1 million profit on day one.

Barclays could do that because that’s how much it estimated it would earn from the LOBO loan over the course of the contract. It’s important to note here that there are only two parties involved in the contract: Barclays and Walsall Council. In other words, that money is coming from Walsall Council.

Based on the responses to Debt Resistance UK Freedom of Information requests to over 200 councils Sachdev further estimates that in total, banks have booked around £1 billion in profits from LOBO loans to UK local authorities.

That’s a billion pounds of profit for banks paid for by council taxes, business rates, parking tickets and the other revenues that councils raise that should be spent on providing essential services, not feathering the nests of the financial elite.

Remember, if the councils had instead taken out loans from the Public Works Loan Board then the interest paid on those loans would have stayed in the public sector instead of acting as a further drain on government finances.

Proponents of austerity tell us, ad nauseum, that our government is too much in debt. If so then surely we’re only exacerbating that problem by paying interest on the debt to bankers instead of to ourselves.

3. LOBO loans are more expensive to arrange than loans from government

When councils take out a loan from the Public Works Loans Board they pay an arrangement fee of 35p for every £1,000 they borrow at a fixed rate of interest and 45p for every £1,000 they borrow at a variable rate of interest with the minimum fee set at £25. So a council borrowing £10 million from the PWLB could expect to pay a maximum of £4,500 to arrange the loan.

When councils take out loans from banks they generally don’t deal with the banks directly. Instead they use the services of interdealer brokers – a specialist breed of city go-betweens – much like you or I might use the services of mortgage broker when buying a home. The broker rings around the banks and then comes back with the ‘best’ deal they could find.

Like a mortgage broker the interdealer broker makes a commission on each deal they secure. In the case of LOBO loans these commissions are very high (the banks are greedy for the business due to the profits outlined above), sometimes approaching 1% of the loan amount. On a loan with a face value of £10 million that would mean a commission of nearly £100k.

But the story doesn’t end there. The interdealer brokers are actually getting paid on both sides of the deal. Debt Resistance UK Freedom of Information requests have revealed that brokers are often also paid around 0.24% of the loan value by the councils themselves. In the case of a £10 million LOBO loan that’s another £24,000 for the broker straight out of the public purse.

We’ve analysed 135 LOBO loan deals where the the broker and the fee have been released under Freedom of Information which leads us to estimate that brokers have earned at least £30 million directly from councils for arranging LOBO deals. That’s on top of over £100 million commission earned from the banks (which councils have probably also paid for, indirectly, because the banks would have just added the commission onto the cost of the loan).

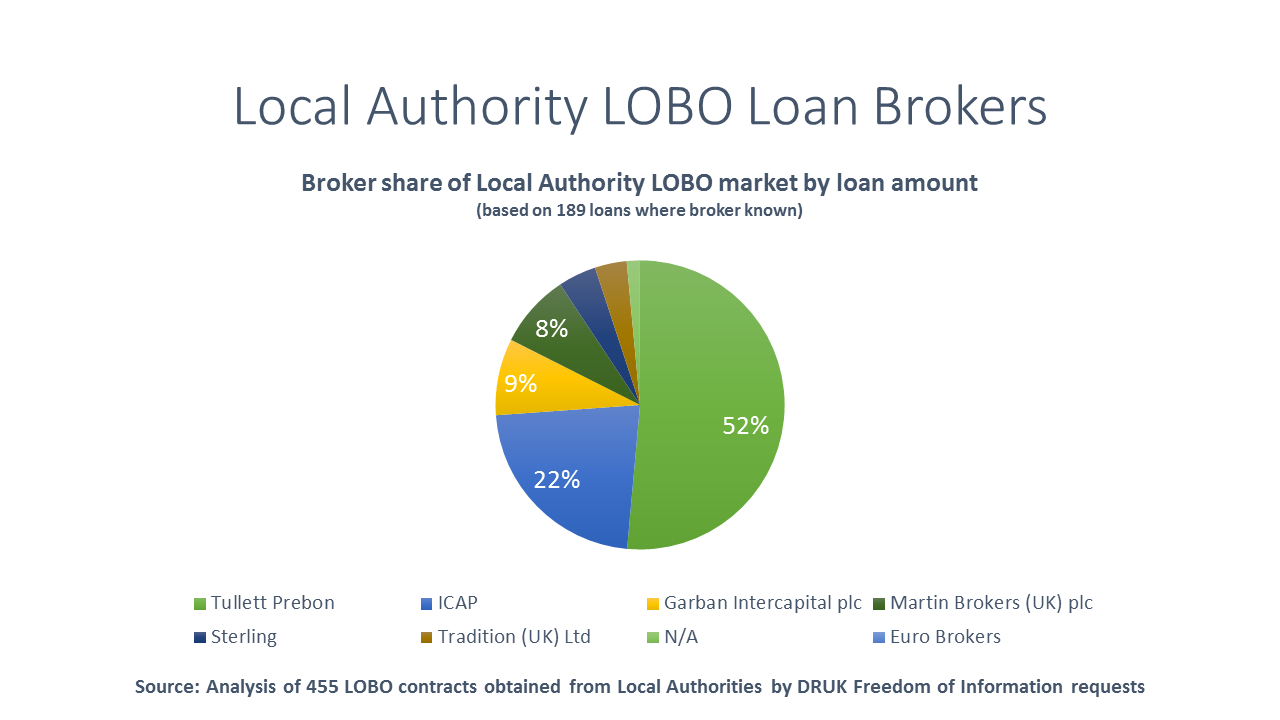

So who are these interdealer brokers benefiting from the public purse to the tunes of tens of millions of pounds?

The most prolific is Tullett Prebon, which brokered 52% of the LOBO deals we’ve seen where the broker was known. Tullett Prebon made the pink papers in July by purchasing MOAB Oil Inc, a US energy broker.

On the board of Tullett Prebon sits Angela Knight, former Conservative MP for Erewash from 1992 to 1997 and former Chief Executive of the British Bankers Association where she led the industry’s shameful defence of PPI ‘mis-selling’.

The second biggest interdealer broker in the LOBO loan market is ICAP. ICAP brokered 22% of all the LOBO loan deals we’ve seen where the broker was known.

Chief Executive of ICAP is Michael Spencer, who’s made it onto the Sunday Times Rich List and who donated more than £2m to the Conservative Party in 2010. Later in 2010, Chancellor George Osborne put up the rates at which councils could borrow from the PWLB.

One of ICAP’s former subsidiaries, Butlers, provided Treasury Management Services to UK local authorities – but we’ll have to leave the role of these so-called Treasury Management Advisors, and their relationships with interdealer brokers, to part 3.

Posted in Blog